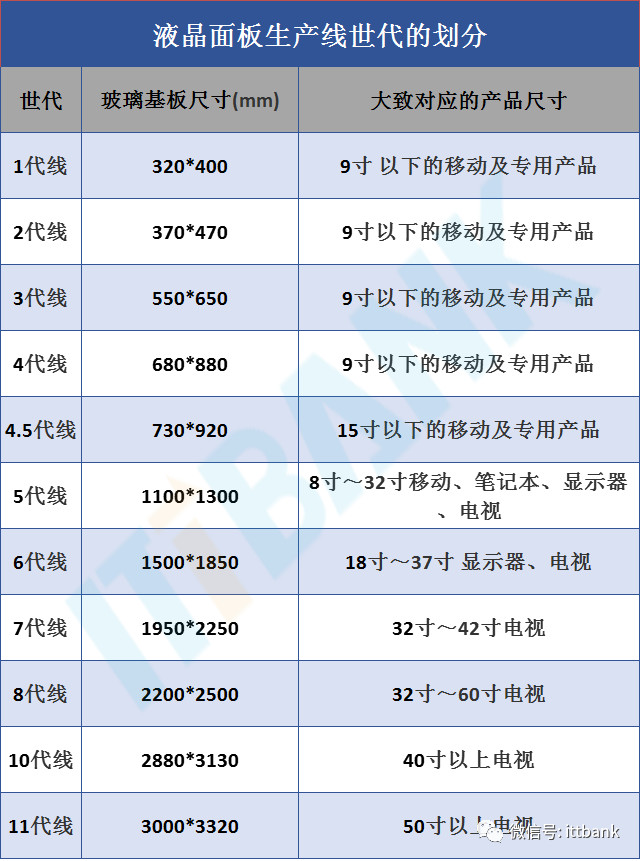

seline;color:#3E3A39;text-indent:0px;"> 先來看一張屏幕分辨率表:

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;"> 液晶麵板行業(ye) 產(chan) 業(ye) 鏈:

seline;color:#3E3A39;text-indent:0px;"> 上遊材料或元件主要包括液晶材料、玻璃基板、偏光片、背光源、自動化設備,光阻材料,膜材料,靶材,化工材料等;中遊則主要是麵板製造廠為(wei) 主的加工製造,主要製程包括清洗,塗布,曝光,蝕刻,電鍍等等。後續製程包括檢查,切割,貼片,模組,成盒等等。通過在玻璃基板上製作TFT陣列和CF基板,將CF作為(wei) 上板和TFT下板自建灌注液晶並貼合,最後再貼上偏光片,連接驅動IC和控製電路板,與(yu) 背光模組進行組裝,最終形成整塊液晶麵板模組;下遊則是以各種領域各類應用終端為(wei) 主的品牌商、組裝廠商等。

seline;color:#3E3A39;text-indent:0px;">

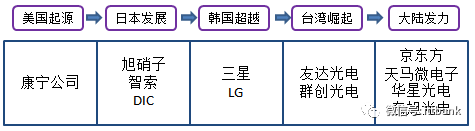

seline;color:#3E3A39;text-indent:0px;"> 目前美國和日本以及德國主要致力於(yu) 行業(ye) 上遊原材料;而韓國、台灣和大陸則主要在行業(ye) 中遊麵板製造環節謀求發展。隨著我國大陸高世代線的相繼投產(chan) ,使得麵板產(chan) 能、技術水平穩步提升,產(chan) 業(ye) 競爭(zheng) 力逐漸增強,如今的麵板產(chan) 業(ye) 韓國、中國大陸、中國台灣三分天下,中國大陸有望在2019年成為(wei) 全球第一。

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲中國崛起為(wei) 全球LCD產(chan) 業(ye) 第三極

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

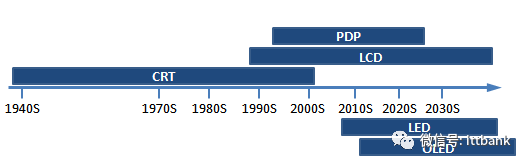

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲各類顯示技術的發展時間軸

seline;color:#3E3A39;text-indent:0px;">

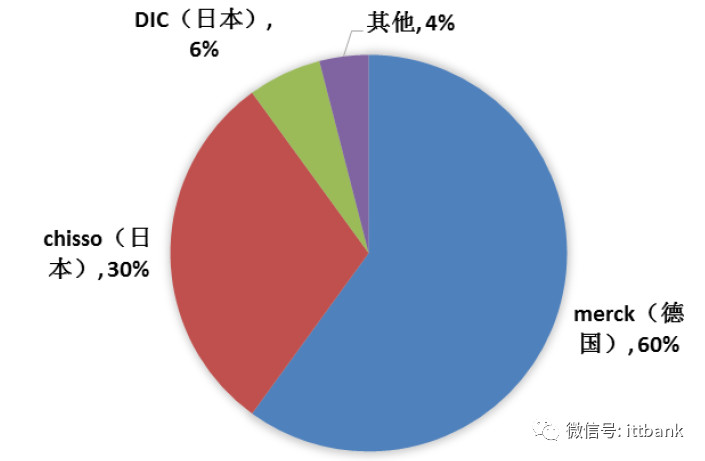

seline;color:#3E3A39;text-indent:0px;"> 液晶材料市場被德、日壟斷

seline;color:#3E3A39;text-indent:0px;"> 液晶分為(wei) 單晶和混晶,任何一種單晶不能直接用於(yu) 顯示,液晶顯示材料配方中需混合10種到20種不同的單晶,我們(men) 稱之為(wei) 混晶。單晶是混晶的必備材料,混晶生產(chan) 商自己生產(chan) 一部分單晶,其餘(yu) 由專(zhuan) 業(ye) 單晶生廠商生產(chan) 。單晶相比於(yu) 混晶的附加價(jia) 值低,生產(chan) 重心已向我國轉移,國內(nei) 生產(chan) 單晶的廠商主要有煙台萬(wan) 潤、西安瑞聯、上海康鵬等。混晶的技術壟斷性較強,被德國Merck、日本Chisso和大日本油墨(DIC)三家占據了市場96%的份額。國內(nei) 從(cong) 事混晶材料的公司主要有誠誌永華和清華亞(ya) 王,產(chan) 品主要用於(yu) 低端市場,約占低端產(chan) 品70%。

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;">

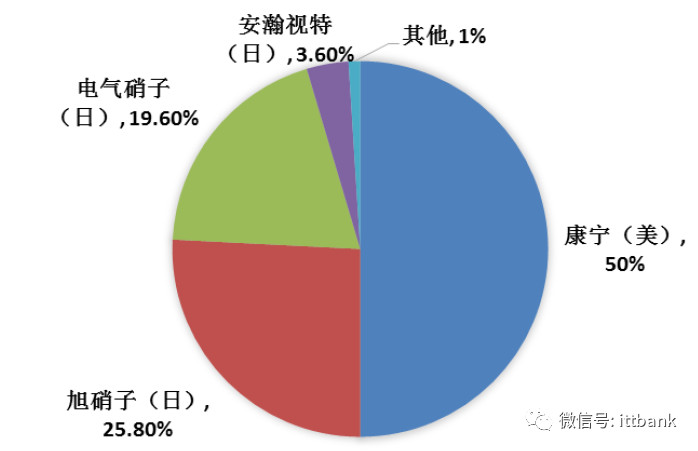

seline;color:#3E3A39;text-indent:0px;"> 玻璃基板市場被美日平分,大陸廠商奮起直追

seline;color:#3E3A39;text-indent:0px;"> 玻璃基板是一種高性能玻璃,是TFT-LCD麵板行業(ye) 上遊最重要的原材料之一,也是運輸成本最高的原材料之一。之所以在產(chan) 業(ye) 鏈中占據如此重要的地位,是因為(wei) 液晶顯示器的分辨率、透光度、重量、視角等都與(yu) 玻璃基板的性能密切相關(guan) 。每一塊TFT-LCD麵板,都需要兩(liang) 片相同大小的玻璃基板,分別用作薄膜電晶體(ti) 基板(TFT基板)和彩色濾光片基板(CF基板)。

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;"> 近幾年TFT-LCD行業(ye) 景氣度持續提升,出貨麵積屢創新高,市場對玻璃基板的需求也與(yu) 日俱增。由於(yu) 投資門檻高、技術風險大,海外玻璃基板企業(ye) 長期對核心技術嚴(yan) 密封鎖,導致國內(nei) 麵板企業(ye) 主要依靠進口解決(jue) 玻璃基板的來源問題。

seline;color:#3E3A39;text-indent:0px;">

全球近200億(yi) 美元的利潤主要被四家廠商瓜分,康寧(包括三星康寧合資公司)約占了全球市場的一半,日本的旭硝子、電氣硝子分別占據了25.8%、19.6%的份額,安翰視特占3.6%。

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲國內(nei) 主要液晶麵板產(chan) 線和玻璃基板來源

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

▲國內(nei) 玻璃基板廠商已建產(chan) 能統計

▲國內(nei) 玻璃基板廠商已建產(chan) 能統計

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;"> 偏光片國產(chan) 化替代加速

seline;color:#3E3A39;text-indent:0px;"> 偏光片市場主要被日韓企業(ye) 壟斷,韓國LG 化學占市場份額27%,日本東(dong) 電工占26%,住友化學占24%。偏光片上遊的主要原材料TAC 膜和PVA 膜更是被日本企業(ye) 牢牢掌控。日本富士占據TAC 薄膜60%以上市場份額,KonICA 占據約20%的市場。日本可樂(le) 裏(Kuarary)占據PVA 薄膜70%以上的市場。目前國內(nei) TFT-LCD用偏光片產(chan) 品仍處於(yu) 發展的初期,當前TFT用偏光片產(chan) 能大約為(wei) 1200萬(wan) 平米,國內(nei) 供給率為(wei) 10%左右,未來國產(chan) 化替代空間巨大。主要的生產(chan) 廠商有深紡織子公司盛波光電和三利普。自2012年起,中國偏光片產(chan) 能占全球總產(chan) 能的比例逐漸升高,2012年該比例僅(jin) 為(wei) 4.3%左右,至2015年則上升至8.8%。全球最大的三家偏光片廠商占據全球產(chan) 能占比逐年下降表明國產(chan) 偏光片正在加速替代,將進一步減少大陸麵板廠商的上遊原材料成本。

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲2016年全球偏光片市場份額

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;"> 背光模組

seline;color:#3E3A39;text-indent:0px;"> 是顯示麵板最貴的部分,占了成本大約20%以上,但是技術難度不高,屬於(yu) 勞動密集型產(chan) 業(ye) ,全球絕大部分背光模組都是在我國生產(chan) 。

seline;color:#3E3A39;text-indent:0px;"> 但是背光模組60%左右的成本來自光學膜,主要包括擴散膜,反射膜,增亮膜等,這方麵國產(chan) 進度還不錯,發展速度很快。國內(nei) 比較專(zhuan) 注擴散膜,反射膜,增亮膜生產(chan) 的寧波激智科技,增長也很快。

seline;color:#3E3A39;text-indent:0px;"> 光學膜國產(chan) 康得新是龍頭主力,已經是世界最大的光學膜生產(chan) 企業(ye) 之一。

seline;color:#3E3A39;text-indent:0px;"> 然而更上遊的材料,國產(chan) 還需要繼續努力 這些光學膜的生產(chan) 主要原料是光學基膜,要生產(chan) 光學膜,就要采購光學基膜,目前在光學基膜方麵,全球80%以上的產(chan) 能由三菱樹脂、東(dong) 麗(li) 、帝人、杜邦、可隆、SKC、東(dong) 洋紡等幾大巨頭所壟斷。國產(chan) 的廠家有樂(le) 凱集團,康得新,裕興(xing) 股份,南洋科技(東(dong) 旭成化學)等等。

seline;color:#3E3A39;text-indent:0px;">

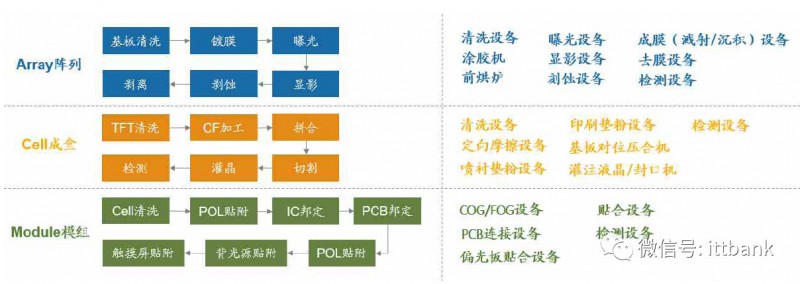

seline;color:#3E3A39;text-indent:0px;"> 麵板自動化設備

seline;color:#3E3A39;text-indent:0px;"> 台灣麵板設備廠商主要專(zhuan) 注LCD麵板後段製程設備及檢測設備。LCD液晶麵板製造

seline;color:#3E3A39;text-indent:0px;"> 主要分為(wei) 三段,前段Array陣列製程、中端Cell成盒製程以及後段Module模組製程。

seline;color:#3E3A39;text-indent:0px;"> 其中前兩(liang) 段工藝製程技術難度較大,目前日本、韓國、美國仍占據著絕對的主導地

seline;color:#3E3A39;text-indent:0px;"> 位;我國台灣地區的麵板設備廠商目前在後段設備已基本實現自主生產(chan) ,並有向中

seline;color:#3E3A39;text-indent:0px;"> 前端拓展的趨勢。此外,檢測設備貫穿整個(ge) 麵板生產(chan) 線,台灣設備廠商在三段製程

seline;color:#3E3A39;text-indent:0px;"> 中均已實現布局。

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲LCD液晶顯示麵板工藝製程及所用設備

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

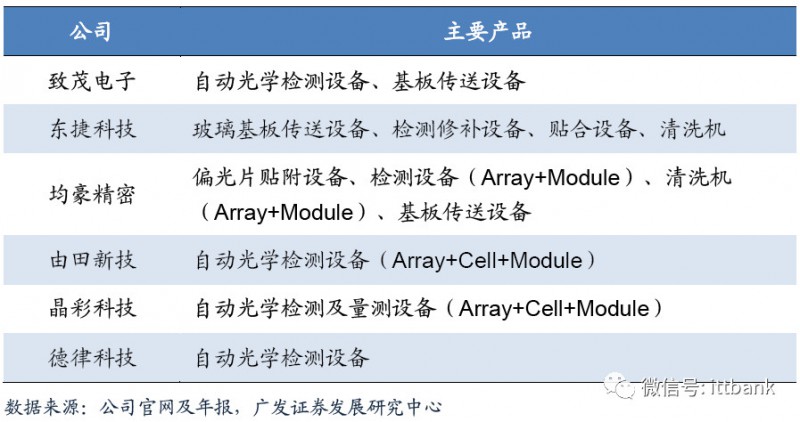

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲台灣地區主要麵板設備廠商及產(chan) 品

seline;color:#3E3A39;text-indent:0px;">

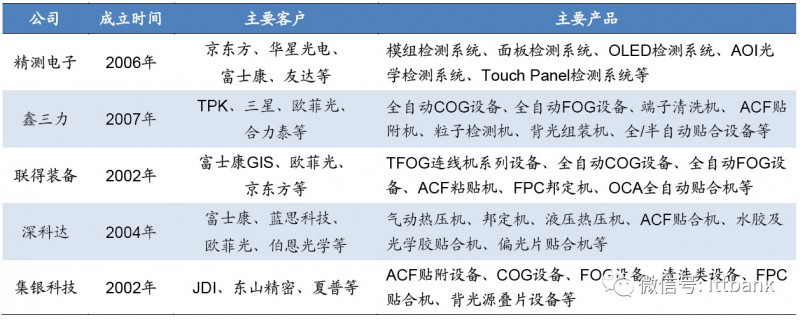

seline;color:#3E3A39;text-indent:0px;"> 與(yu) 台灣設備廠商切入的角度類似,大陸麵板設備廠商也是從(cong) 後段模組製程設備及檢

seline;color:#3E3A39;text-indent:0px;"> 測設備起步。目前大陸麵板設備廠商發展較快的企業(ye) 包括:專(zhuan) 注麵板設備檢測國內(nei)

seline;color:#3E3A39;text-indent:0px;"> 龍頭精測電子,以及在後段模組製程設備的主要供應商鑫三力(智雲(yun) 股份子公司)、

seline;color:#3E3A39;text-indent:0px;"> 聯得裝備、深科達及集銀科技(正業(ye) 科技子公司)、太原風華(未上市)等幾家廠商。

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲中國大陸主要麵板設備廠商及產(chan) 品信息

seline;color:#3E3A39;text-indent:0px;">

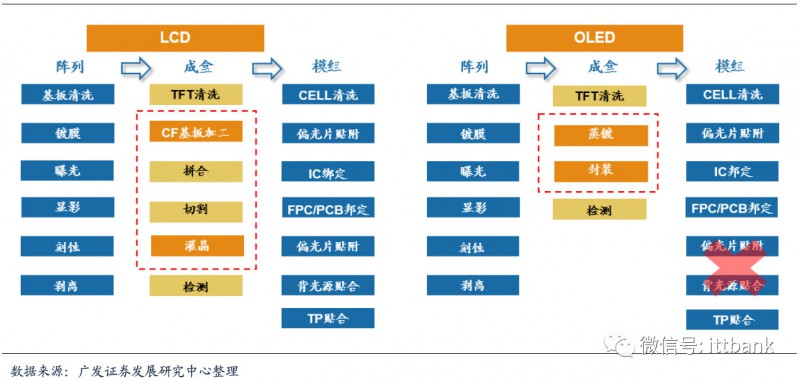

seline;color:#3E3A39;text-indent:0px;"> OLED將成為(wei) 未來的主流顯示技術

seline;color:#3E3A39;text-indent:0px;"> 由於(yu) 小尺寸OLED技術的不斷發展,良率不斷提升,成本逐漸下降,產(chan) 能的陸續釋放,在手機應用端已經出現了OLED代替的趨勢。而電視端目前依然是LCD為(wei) 主,市場上高端電視的代表就是OLED和量子點,其中量子點的推廣廠商主要包括三星、索尼、TCL等廠商,OLED則由LG力推,長虹、康佳等跟進。量子點技術目前依然處於(yu) 發展之中,現有的量子點電視依然依托於(yu) LCD液晶麵板,利用藍光LED作為(wei) 背光源,通過量子點材料介質後與(yu) 其中的納米顆粒發生反應後,發出像素三色光源,改善了傳(chuan) 統LCD液晶電視色域低的缺點,並大大提升了亮度,甚至可以媲美OLED電視。但量子點的本質依然是優(you) 化了的LCD,需要背光,且無法做成柔性顯示,屬於(yu) 一種“折中”方案的技術,隨著QLED的出現,未來量子點技術也將朝著自發光的方向發展。

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

seline;color:#3E3A39;text-indent:0px;text-align:center;"> ▲LCD及OLED顯示麵板工藝製程對比

seline;color:#3E3A39;text-indent:0px;">

seline;color:#3E3A39;text-indent:0px;text-align:center;">

轉載請注明出處。

相關文章

相關文章

熱門資訊

熱門資訊

精彩導讀

精彩導讀

關注我們

關注我們